Pakistan Centre for Philanthropy (PCP) is a designated Certification Agency by the Federal Board of Revenue (FBR), Government of Pakistan. In accordance with the Section 2(36) of Income Tax Ordinance, 2001, organizations working in Pakistan are required to seek approval of Commissioner Inland Revenue to be recognized as not for profit. As part of the procedural requirement as envisaged and provided in rules 211(2)(g), 213 (2)(d), 217 (1) (b)(vii), 220(1)(b)(vi), 220 A (3) (d) and 220 A(7)(1)(b)(iv) of Income Tax Rules 2002 , PCP conducts performance evaluation of NPOs on behalf of FBR and certifies that NPOs/NGOs/CSOs meet with the desired requirements of certification standards.

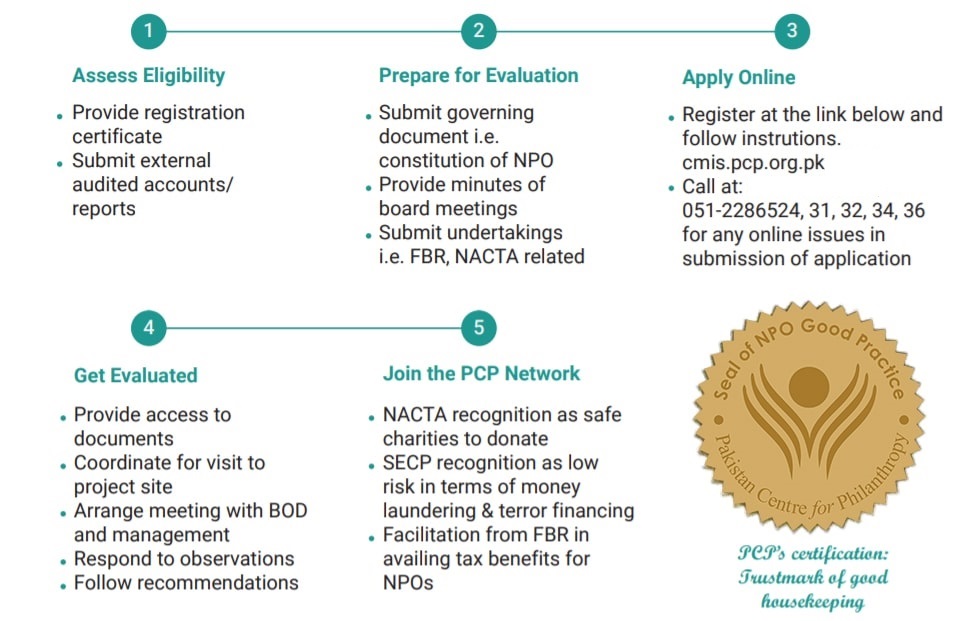

Eligible Organizations

⦁ Non-Governmental Organizations (NGO)/Not for Profit Organizations (NPO)/Civil Society Organizations (CSOs) ⦁ International Non-Governmental Organizations (INGOs) ⦁ Private Universities or Degree Awarding Institutions ⦁ Micro Finance Institutions (MFIs) ⦁ Local Support Organizations (LSOs)

Strengthen your organization and showcase your excellence through PCP Certification Program

PCP is the first Not for Profit (NPO) Certification Agency in Pakistan. PCP Certification System was established in 2003 authorized by the Revenue Division of the Government of Pakistan. Through its certification program, PCP provides accreditation to NPOs which demonstrate excellence and leadership in the following areas of operations;

⦁ Legal & Regulatory Compliance

⦁ General Public Utility Compliance

⦁ Institutional Mechanisms of Oversight

⦁ Compliance with Tax Laws

⦁ Financial Management

⦁ Organizational Policies

⦁ Program Delivery

Why join the certification program?

Invest in credibility and donor confidence with PCP Certification Program trust mark. It helps you learn how to identify and mitigate organizational risk, improve governance practices, promote financial transparency and accountability, and foster a strong workforce.

Five steps to attain Certification

BENEFITS

Tax Benefits

Total Benefits

Collection of tax at imports.

Withholding from dividend income.

Withholding on interest income from national saving schemes.

Withholding on interest income from bank accounts.

Withholding on interest income from loans & borrowings.

Withholding from payment of goods, services and contracts.